How to safely lend money in the Philippines?

Safely lending money in the Philippines requires a cautious approach and adherence to certain practices. One of the key steps is conducting thorough due diligence on the borrower. This involves researching their creditworthiness, financial stability, and repayment capacity. Request necessary documentation such as identification cards, income proofs, and bank statements to verify the borrower’s information. It is also advisable to obtain references or conduct background checks to validate their credibility.

Furthermore, setting clear and reasonable loan terms is essential for safe lending. This includes determining the loan amount, interest rate, repayment schedule, and any associated fees or penalties. Ensure that the terms are fair to both parties and comply with the regulations set by the Bangko Sentral ng Pilipinas (BSP) and other relevant authorities. Communicate the terms clearly to the borrower and address any questions or concerns they may have.

What considerations to keep in mind for secure money lending in the Philippines?

Secure money lending in the Philippines requires careful consideration of several factors. First and foremost, assess the borrower’s ability to repay the loan. Evaluate their income, expenses, existing debts, and overall financial stability. This assessment helps determine the borrower’s capacity to fulfill their repayment obligations.

In addition, it is important to establish effective risk management strategies. Diversify your lending portfolio by offering loans to borrowers from different industries or sectors. Set appropriate loan limits based on your risk tolerance and available resources. Implement a robust loan monitoring and collection process to ensure timely repayments and address any issues promptly. Stay informed about market conditions, economic trends, and regulatory changes that may impact lending activities.

Lastly, maintaining a strong and transparent relationship with borrowers is crucial. Clearly communicate the terms and conditions of the loan, including any potential risks involved. Provide regular updates and reminders regarding repayment schedules. Establish open lines of communication to address any concerns or difficulties faced by borrowers and work together to find suitable solutions.

How to understand the legal requirements for lending money in the Philippines?

Understanding the legal requirements for lending money in the Philippines is paramount to ensure compliance and protect both lenders and borrowers. Familiarize yourself with the regulations established by the BSP, such as the Truth in Lending Act (TILA) and the Anti-Usury Law. These laws govern lending practices, interest rates, disclosures, and consumer protection.

To gain a comprehensive understanding of the legal framework, consider consulting legal professionals financial advisors such as Themis Partners that are specialized in lending laws. They can provide guidance tailored to your specific lending activities and help navigate through the complexities of the regulatory landscape.

Additionally, stay updated on any amendments or revisions to the lending regulations. Regularly review the BSP’s official website, attend industry conferences or seminars, and engage in discussions with other lenders to stay informed about the latest legal requirements and best practices.

By proactively ensuring compliance with the legal framework, lenders can mitigate legal risks, maintain their reputation, and contribute to a responsible lending ecosystem in the Philippines.

What loan options are available in the Philippines?

The Philippines offers various loan options to cater to different financial needs. Some common loan types include personal loans, business loans, housing loans, car loans, and microfinance loans. Each loan agreement type has its own eligibility criteria, interest rates, and repayment terms.

Personal loans are flexible and can be used for various purposes such as debt consolidation, medical expenses, or home renovations. Business loans are specifically designed to support entrepreneurs and SMEs in expanding their operations or addressing capital requirements. Housing loans help individuals or families in purchasing or building their dream homes. Car loans provide financing for the purchase of vehicles. Microfinance loans are small loans typically extended to individuals who may not have access to traditional banking services.

When exploring loan options, it’s important to consider the interest rates, fees, and repayment terms offered by different lenders. Compare the loan terms, evaluate the total cost of borrowing, and assess the lender’s reputation and reliability. It’s advisable to read and understand the loan agreement thoroughly, including the terms and conditions, before committing to any loan.

How to evaluate borrowers in the Philippines and manage risk?

Evaluating borrowers in the Philippines is a critical step in managing lending risk. Start by assessing the borrower’s creditworthiness through a thorough review of their financial history, credit score, and repayment behavior. Consider their income stability, employment history, and existing financial obligations. It’s also important to verify their identity and address to ensure the borrower’s authenticity.

To further mitigate risk, consider requesting collateral or guarantors for the loan. Collateral provides security in case the borrower defaults on the loan, while guarantors offer an additional layer of assurance for repayment. Conduct proper valuation and documentation of collateral assets to safeguard the lender’s interests.

Implementing a robust loan monitoring system is essential to track the borrower’s repayment progress and identify any potential risks or issues. Regularly review loan accounts, monitor payment patterns, and promptly address any delinquencies or defaults. Maintain open communication with borrowers to address any challenges they may face and explore suitable solutions.

It’s crucial to strike a balance between offering accessible financing and managing lending risks effectively. Implementing sound risk management practices, conducting thorough evaluations, and maintaining proactive loan monitoring can help lenders minimize potential risks and ensure a healthy lending portfolio.

What is the documentation process for lending money in the Philippines?

The documentation process for lending money in the Philippines involves gathering and verifying various legal documents to ensure compliance with legal requirements and establish a clear loan agreement. While specific documentation may vary depending on the type and purpose of the loan, there are common documents typically required.

For individuals, lenders typically require identification documents such as a valid government-issued ID (e.g., passport, driver’s license, or social security ID), proof of income (pay slips, employment contract, or income tax returns), and proof of address (utility bills or residency certificates).

For businesses or self-employed individuals, additional documents such as business registration papers, financial statements, and tax returns may be required. Collateral-related documents, such as property titles or vehicle registration papers, may also be necessary for secured loans.

It’s important to carefully review and verify all submitted documents to ensure their authenticity and accuracy. Compliance with the requirements set by the BSP and other regulatory bodies is crucial to ensure a legally binding loan agreement and protect the interests of both parties involved.

By following a thorough documentation process, lenders can establish a transparent and enforceable loan agreement that outlines the rights and responsibilities of both the lender and borrower.

How do loan agreements protect your interests in responsible lending?

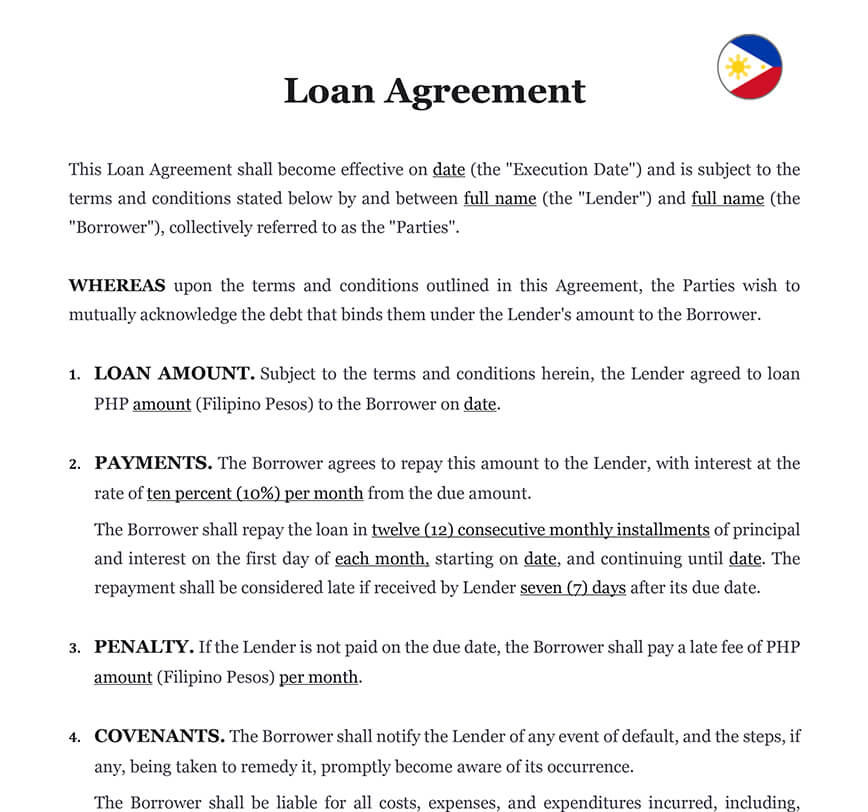

1. Clarity on Loan Terms: Loan agreements specify the loan amount, interest rate, repayment schedule, and any additional fees or charges. By clearly defining these terms, both the lender and borrower have a mutual understanding of their obligations and rights throughout the loan term.

2. Repayment Structure: Loan agreements outline the repayment structure, including the frequency of payments and the duration of the loan. This helps borrowers plan their finances and ensures that they are aware of their repayment responsibilities. For lenders, the repayment structure allows them to monitor and track the repayment progress.

3. Security and Collateral: In cases where loans are secured by collateral, loan agreements detail the collateral requirements and the conditions under which the collateral can be utilized or repossessed in the event of default. This provides added security for lenders and helps mitigate risk.

4. Default and Remedies: Loan agreements define the consequences of default, including late payment penalties and the actions that lenders can take to recover the outstanding loan amount. This gives lenders the ability to take legal action or enforce their rights in the event of non-payment.

5. Dispute Resolution: Loan agreements typically include provisions for dispute resolution, such as arbitration or mediation, which offer a fair and efficient way to resolve conflicts between the lender and borrower. This helps protect both parties’ interests and provides a mechanism for resolving disagreements without resorting to costly and time-consuming litigation.

Loan agreements are legally enforceable documents that provide a framework for responsible lending. They offer protection to both lenders and borrowers by establishing clear terms, outlining repayment obligations, and defining the consequences of default. It’s important for both parties to carefully review and understand the loan agreement before signing to ensure transparency and a mutually beneficial lending relationship.

Ask our Experts to assist you when you lend money in the Philippines

310 client reviews (4.8/5) ⭐⭐⭐⭐⭐